September 7, 2023

Gary Schlossberg, Global Strategist

Jennifer Timmerman, Investment Strategy Analyst

John LaForge, Head of Global Real Asset Strategy

The U.S. dollar’s future as the world’s reserve currency

Key takeaways

- Although global “de-dollarization” periodically dominates headlines, we do not foresee a meaningful risk of the greenback losing its status as the world’s primary reserve currency (that is, the main currency for international trade and investment).

- In our view, the U.S. dollar’s deep-seated advantages — including the rule of law, transparency, and a highly liquid financial market — make a global shift away from the U.S. dollar extremely difficult.

What it may mean for investors

- We continue to favor allocating most of a portfolio’s available long-term capital to U.S. dollar-denominated equities and fixed income, along with some international financial market diversification and commodity exposure.

- For portfolios allocated in these ways, we prefer to avoid adjustments triggered by speculation that the U.S. dollar may be in danger of losing its premier reserve currency status at the hands of some new challenger that lacks the qualifications and the staying power.

Threats to the U.S. dollar’s key-currency status are decades old and have included the 1971 collapse of the gold-exchange standard and the advent of floating exchange rates, fears of global banking collapse in 2008, and worries about U.S. policy miscues. None has removed the dollar from its leadership position.

The latest round of challenges include:

- China’s growing importance to the global economy, now top-ranked in foreign trade and moving aggressively to shore up support for the yuan’s international role.1

- Technological advances fostering the rise of cryptocurrencies and central bank digital currencies (CBDCs), prompting talk (erroneously, we think) of a new front against the U.S. dollar’s international status.

- Geopolitical tensions and fears of actual or potential U.S. financial sanctions are accelerating efforts to diversify out of the U.S. currency by China and other targets of U.S. economic sanctions. One outgrowth of that response has been a recent agreement among Saudi Arabia, China, and Russia to price some oil transactions in Chinese yuan. (Beyond any benefit of payments diversification, the Saudis may feel alternate payments currencies, like the yuan, allow them to maintain access to important markets vulnerable to U.S. sanctions.)

This report explores the reasons for the U.S. dollar's enduring role as the global economy's dominant international currency. First, it facilitates global trade, lending, and investment. Second, the dollar is uniquely qualified for this role, in our view. And third, despite headlines that announce replacements for the dollar, the weaknesses in other currencies likely will prevent them from successfully challenging the dollar as the world's main reserve currency.

The world’s financial plumbing runs on the U.S. dollar

Global currency status is anchored by the U.S. dollar’s integral role in global financial plumbing (by which we mean its role in international trade finance, borrowing, and global investment). According to data from the Bank for International Settlements (BIS, a clearinghouse for global central bank transactions), over $7.5 trillion in foreign exchange trades occur every day, and 90% of that turnover involves the dollar.2 The dollar’s share is 50% of cross-border loans, international trade in debt securities, and trade invoicing.3

Adding to the greenback’s allure in the past decade have been the attractive yields on dollar assets, due in large measure to more rapid economic growth in the U.S. compared to other money-center countries. Since 2014, for example, yields on 10-year Treasury notes have never been less than a percentage point above yields on comparable German government securities.

Of course, other currencies have a role. Individual countries can and do use their own currencies in bilateral trade. The dollar’s share of total world trade is only 10%, and the U.S. dollar accounts for only 20% of global economic output as the world has become wealthier.4 Even so, the U.S. dollar remains the dominant currency for countries whose currencies are thinly traded. For example, an Argentine wine producer is likely to invoice a Taiwanese wine buyer in U.S. dollars, because neither the Argentine peso nor the Taiwanese dollar will be easy or cheap for either party to exchange. The U.S. dollar’s liquidity and availability make it the cheapest and most accessible currency for billing and payment, even if no U.S. citizen is a party to the transaction.

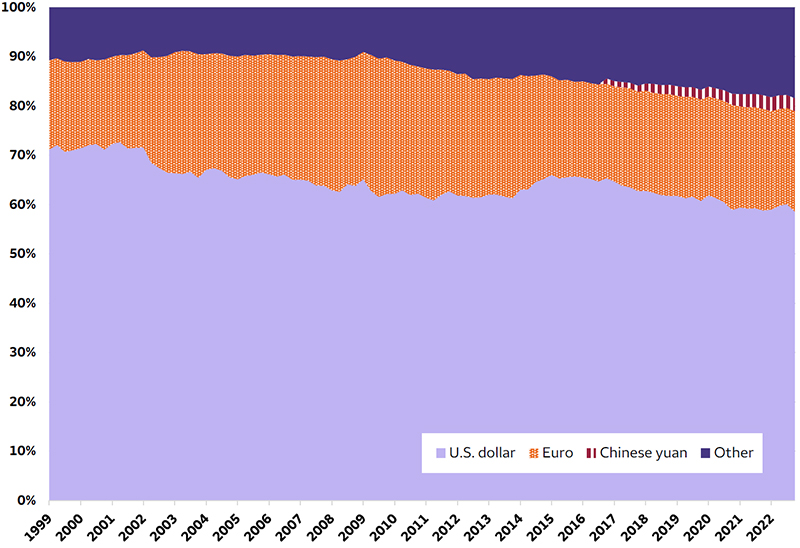

In addition, the growth in global trade connections and wealth have encouraged governments to diversify their foreign exchange reserves — liquid assets that hold their value and that governments and central banks keep in case of emergencies. Chart 1 shows that the U.S. dollar's share in global currency reserves has declined since 1990, in favor of an array of alternatives, consistent with diversification and, we suppose, national priorities arising from growing bilateral trading arrangements. The euro and the Chinese yuan are prominent challengers to the dollar in reserves but have failed to attract larger reserve shares in recent years. Bottom line: Even if other currencies are now more useful than they were decades ago, the U.S. dollar remains indispensable for running the world’s financial plumbing.

Sources: Wells Fargo Investment Institute and International Monetary Fund (IMF) Currency Composition of Official Foreign Exchange Reserves (COFER) data, as of December 31, 2022; Quarterly data: March 31, 1999 to December 31, 2022.

Sources: Wells Fargo Investment Institute and International Monetary Fund (IMF) Currency Composition of Official Foreign Exchange Reserves (COFER) data, as of December 31, 2022; Quarterly data: March 31, 1999 to December 31, 2022.What makes premier reserve currency status?

As we suggested earlier in this report, there are several essential attributes of an international currency:

- Does it have a central role in pricing international trade and financial transactions?

- Is it used as a payment vehicle, or medium of exchange in those transactions?

- Perhaps most importantly, does it draw support for its role as a financial-transactions vehicle from its use as a store of value for financial-asset accumulation by private investors, central banks, the International Monetary Fund, and other multilateral institutions?

Only the U.S. dollar checks all the boxes for the key global currency, dating back to the 1960s, and, in our view, extending well into the future:

- Depth and liquidity of U.S. financial markets

The depth, liquidity, transparency, and reliable governance of U.S. markets have made the U.S. dollar the most efficient vehicle for financial transactions, which, in turn reinforces that role as a store of value essential for an international currency. - The U.S. dollar’s visibility in financial transactions and as an investment destination helps cement its role as a unit of value, or pricing standard, in trade and finance and as a medium of exchange

Convention supporting the dollar’s role as a pricing and payments vehicle is deepened materially by a ubiquitous presence in global financial transactions, underpinned by a reputable banking system, the rule of law, and transparency based on sound corporate governance. - The U.S. dollar as a national currency, backed by a single, identifiable national authority

National-currency status distinguishes the dollar from a supranational currency (like the euro), with clear sovereign backing assuring the currency’s stability and longevity. - The U.S. dollar’s unique role during times of global stress

Attributes summarized above support the U.S. dollar’s role as an important perceived haven asset — above all others — during times of crisis. This can largely be ascribed to the fact that the U.S. central bank historically has been able to move swiftly to respond as the “global firefighter” by pumping liquidity into global markets. During times of financial stress, the Federal Reserve has regularly opened U.S. dollar swap lines with major developed central banks to provide globally recognized liquidity, offering clear evidence of U.S. institutional strength and proof of constant global demand for dollars. - The U.S. dollar’s greater flexibility in managing credit to accommodate non-inflationary — and deflationary — demands of global trade and investment

Gold seems like an attractive anchor for a global currency system, but that link means the money supply cannot grow faster than the growth in the world’s gold supply, which has averaged only 1.83% from 1900 – 2022.5 The U.S. dollar, or any fiat currency, provides greater flexibility to meet the financing needs of an expanding global economy.

Likewise, a country willing to serve as the world’s banker must be willing to strike a fine balance between its own budget deficit and its economy’s trade balance. Surpluses, or insufficient deficits, can leave the world with a deflationary shortage of dollars, just as when the U.S. was running consistent balance-of-payments surpluses during the early post-World War II period in the 1950s. Excessively large budget and balance of payments deficits risk undermining confidence in the dollar by flooding the world economy with the currency, as in the 1970s. Getting the balance of supply just right can reinforce the greenback’s dominant international role by enhancing powerful “network effects” already in place.6

Challengers to the U.S. dollar’s dominance fail the qualifications

The euro

The euro is currently the only serious contender for the U.S. dollar’s role (see Chart 1), as it possesses a deep, regional financial market and many of the other prerequisites for an international currency mentioned earlier. However, its principal drawback is that it remains a supranational currency, lacking a single national authority to back its viability or ensure its stability. This weakness became apparent during the euro crisis in the aftermath of the Great Recession, when a euro breakup seemed a real possibility. The debate over the euro’s future centered around insufficient economic convergence on eurozone-wide standards for national government spending and debt levels, which is critical to any common currency. It remains a cautionary tale for any group of countries that proposes a supranational currency without first firmly agreeing to surrender control of their national policies for the good of the group.

The Chinese yuan

Although the Chinese yuan is most often cited as the primary threat to the U.S. dollar, its consistently small share of global currency reserves (see Chart 1) is at odds with China's rank as the second largest economy in the world. In our view, broader adoption of the Chinese yuan will remain constrained by China’s dependence on capital controls as a policy tool to dampen its exchange rate and financial turbulence. The nation’s governance, policy track record, and lack of transparency remain a serious hindrance to global adoption — despite one of the largest bond markets in the world — and this is unlikely to improve anytime soon. At best, we believe the Chinese yuan’s international role remains nascent, despite its important role in global trade.

A commodity-backed currency

The method of pegging a currency’s value to any commodity (or basket of commodities) immediately restricts the ability of the participating countries to expand credit — unless they can increase the supply of the commodities. If the country is small, then local conditions may make the economy susceptible to swings between inflation and deflation, as commodity revenue rises and falls. Finally, any commodity is by nature finite and scattered. Accumulating more can prove extremely difficult. (Consider the rarity of major gold finds.) This fatal flaw is why, in the aftermath of World War I, countries broke from the commodity-currency gold standard and its deflationary consequences, helping make depressions much less common now than they once were.

A supranational bloc of emerging-market countries

Specifically, the BRICS nations — Brazil, Russia, India, China, and South Africa — have proposed to add members and challenge the financial system organized by the U.S. and other developed-market countries. We view such a challenge as improbable. The policy coordination among these countries appears more of a distant goal than a current reality. China, for example, has been seeking to replace the dollar in its trade, while India has pushed back against the idea of a common currency altogether.7 Such internal policy disagreements are very likely to multiply the more the BRICS alliance expands. As with the euro 15 years ago, conflicting national and international goals of a broader membership are a main threat to the economic cohesion of a group of countries.

The strengths of the potential would-be members in Latin America, Africa, and most of Asia (except India and China) are population growth and commodities, but we do not believe these strengths will produce a group strong enough to displace the U.S. dollar in global finance. Historically, commodity prices have gone through wide swings that encourage unsustainable spending while commodity revenues are rising, and policy reversals and political instability when the cash flow dries up. We expect further wide swings in the coming decade. And commodities are largely homogeneous goods, so group members would have to set aside their natural competition as suppliers. Population growth also can be an advantage, but not if educational systems and working tools are inadequate, the legal system lacks transparency, and foreign investment waxes and wanes with commodity price trends. Groupings like an expanded BRICS bear watching, but being against something (Western financial system rules) is unlikely to be sufficient common ground to create a group that is more attractive together than its members are for facilitating global financial transactions.

The petroyuan

Also on our radar is the development of a petroyuan — China’s proposal to trade oil for Chinese yuan with the Gulf Cooperation Council (GCC), led by Saudi Arabia. It is not unusual to see countries trade with China in yuan. In fact, Brazil and Argentina already do. Whether the GCC would price all its oil in yuan may depend on U.S. foreign policy over the next few years. The U.S. opposes the GCC’s move to trade oil for Chinese yuan and remains the primary security provider for the group against Iran’s bid to dominate the Middle East. The U.S. also supports and helped negotiate the Abraham Accords, 2020 agreements that help establish economic cooperation between Israel and Middle Eastern states. Thus, we doubt that the GCC countries would completely shift their diplomatic and economic orientation away from the U.S. and its allies to price all its oil in yuan.

A central bank digital currency (CBDC)

A recent survey of 86 of the world’s central banks by the Bank for International Settlements (BIS) — effectively a forum for the world’s central bankers — showed that 93% were involved in some form of CBDC work.8 The CBDC, a direct liability of the central bank (as opposed to traditional money, which is a liability of commercial banks), effectively circumvents the banking system. CBDC development aims to increase the speed of international payments. CBDCs potentially could encroach on the dollar’s role as a pricing mechanism and as a medium of exchange, if central banks use them to settle payments with each other directly, instead of using the global commercial banking system.

Ultimately, however, CBDCs of China and others seeking to internationalize currencies would face the same hurdles as their traditional paper counterparts. These include transparency requirements, governance, and market infrastructure supporting the dollar’s unique role in the global financial system. Even less clear is the CBDC’s threat to the U.S. dollar’s role as a pricing unit of account and, more importantly, its use as a store of value without the deep, well-developed capital market to support financial transactions.

Investment implications

Each headline about some new threat to the U.S. dollar’s status prompts us to fully consider the challenger’s qualifications. We do expect more trade among emerging-market countries, with more use of local currencies in bilateral trade, but we believe that no other currency, collection of currencies, or commodity-based currency meets every key qualification to replace the U.S. dollar's dominant role in international finance, or become the cheapest and most available currency for two countries whose currencies are thinly traded. All these aspirants face their own structural defects, as well. These include usually arbitrary and opaque policies, capital controls, and, at times, a lack of clear government rules and regulations of the banking system. Such deficiencies should continue to undermine long-term exchange rate stability and discourage their global use.

Like all currencies, the U.S. dollar’s value ebbs and flows with economic variables, such as interest rates and the relative strength of the U.S. economy in the world. But our research finds that these cyclical variations have not dented the dollar’s unmatched value for global borrowing, payments, and investment flows. We do not envisage a negative long-run backdrop for the U.S. currency resulting in market turbulence sufficient to dethrone the dollar, or to generate international financial market instability.

For long-term investors whose savings are primarily in U.S. dollars, we continue to favor allocating most of the available capital to dollar-denominated equities and fixed income. Some international financial market diversification may generate higher returns and may moderate swings in portfolio values at times when the global economy outpaces the U.S. economy. Especially for conservative U.S. investors, positions in U.S. multinationals may provide capital appreciation and dividends, while allowing the company to manage exchange rate exposure. For portfolios allocated in these ways, we prefer to avoid adjustments triggered by speculation that the U.S. dollar may be on the verge of losing its premier reserve currency status at the hands of some new challenger that lacks the qualifications and the staying power.

1 United Nations Conference on Trade and Development (UNCTAD), “China: The rise of a trade titan,” April 2021.

2 Bank for International Settlements, “OTC foreign exchange turnover, April 2022,” part of a triennial central bank survey, published in October 2022.

3 Ibid

4 Bank for International Settlements Quarterly Review, December 2022.

5 Source: U.S. Geological Survey global production data (2023).

6 “A phenomenon whereby a product or service gains additional value as more people use it,” according to Oxford Languages.

7 “BRICS plan to float a common currency & India's reaction to it,” Times of India, July 8, 2023. Regarding China, see “De-dollarization has started, but the odds that China's yuan will take over are 'profoundly unlikely to essentially impossible',” Market Insider, July 2023.

8 Anneke Kosse and Ilaria Mattei, BIS Papers No. 136, “Making Headway—Results of the 2022 BIS Survey on central bank digital currencies and crypto,” Monetary and Economic Department, BIS, July 2023.

Risk Considerations

Different investments offer different levels of potential return and market risk. The level of risk associated with a particular investment or asset class generally correlates with the level of return the investment or asset class might achieve. Stock markets, especially foreign markets, are volatile. Stock values may fluctuate in response to general economic and market conditions, the prospects of individual companies, and industry sectors. Foreign investing has additional risks including those associated with currency fluctuation, political and economic instability, and different accounting standards. These risks are heightened in emerging markets. Bonds are subject to market, interest rate, price, credit/default, liquidity, inflation and other risks. Prices tend to be inversely affected by changes in interest rates. The commodities markets are considered speculative, carry substantial risks, and have experienced periods of extreme volatility. Investing in a volatile and uncertain commodities market may cause a portfolio to rapidly increase or decrease in value which may result in greater share price volatility.

General Disclosures

Global Investment Strategy (GIS) is a division of Wells Fargo Investment Institute, Inc. (WFII). WFII is a registered investment adviser and wholly owned subsidiary of Wells Fargo Bank, N.A., a bank affiliate of Wells Fargo & Company.

The information in this report was prepared by Global Investment Strategy. Opinions represent GIS’ opinion as of the date of this report and are for general information purposes only and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally. GIS does not undertake to advise you of any change in its opinions or the information contained in this report. Wells Fargo & Company affiliates may issue reports or have opinions that are inconsistent with, and reach different conclusions from, this report.

The information contained herein constitutes general information and is not directed to, designed for, or individually tailored to, any particular investor or potential investor. This report is not intended to be a client-specific suitability or best interest analysis or recommendation, an offer to participate in any investment, or a recommendation to buy, hold or sell securities. Do not use this report as the sole basis for investment decisions. Do not select an asset class or investment product based on performance alone. Consider all relevant information, including your existing portfolio, investment objectives, risk tolerance, liquidity needs and investment time horizon. The material contained herein has been prepared from sources and data we believe to be reliable but we make no guarantee to its accuracy or completeness.

Wells Fargo Advisors is registered with the U.S. Securities and Exchange Commission and the Financial Industry Regulatory Authority, but is not licensed or registered with any financial services regulatory authority outside of the U.S. Non-U.S. residents who maintain U.S.-based financial services account(s) with Wells Fargo Advisors may not be afforded certain protections conferred by legislation and regulations in their country of residence in respect of any investments, investment transactions or communications made with Wells Fargo Advisors.

Wells Fargo Advisors is a trade name used by Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC, Members SIPC, separate registered broker-dealers and non-bank affiliates of Wells Fargo & Company.